The Great Decoupling

What Google’s 2026 Announcement Signals for Lead Generation

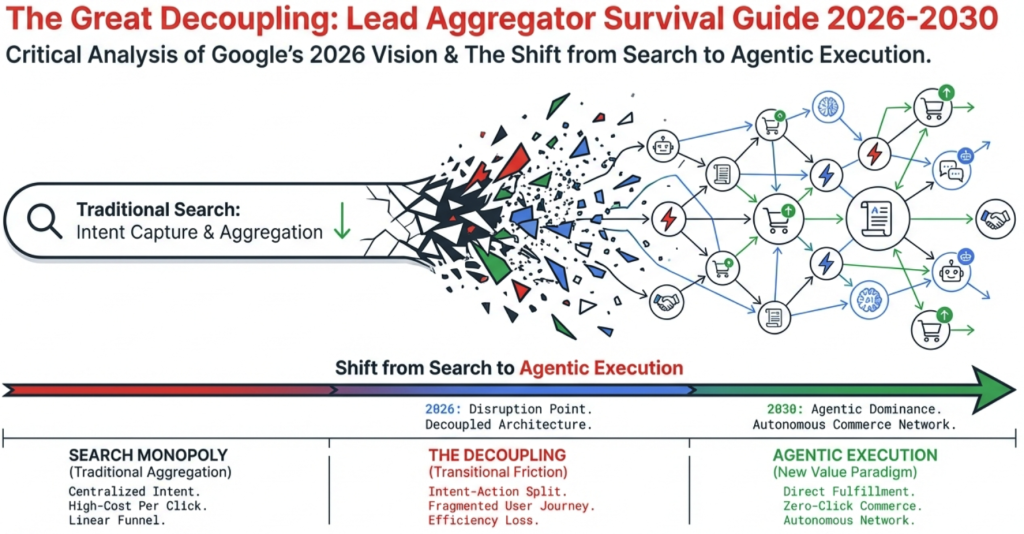

I’ve been reflecting on Google’s February 11th announcement. Not on the feature set, but on the direction.

What stands out is not AI search. It is compression.

Over the past five years, Google has progressively absorbed layers of the advertising and commerce stack – bidding, creative, optimization, measurement, and checkout. The latest shift extends into comparison and transaction routing. For lead generation businesses, comparison is the economic layer. That is where the structural pressure now sits.

A Five-Year Pattern of Vertical Integration

This development did not begin in 2026.

In 2021-22, Performance Max reduced advertiser control and consolidated inventory under automated systems. In 2023-24, AI Overviews began satisfying informational intent directly within search results, and traffic to third-party sites started bleeding. By 2025, AI-driven bidding and closed-loop infrastructure had matured through AI Max and the Agent Payments Protocol (AP2). Now in 2026, the Universal Commerce Protocol (UCP) introduces structured, machine-readable offers and in-platform transaction capability.

Each phase incrementally reduced reliance on outbound clicks and external comparison surfaces. Search volume remains strong, but click dependency is weakening. For platforms, this is efficiency expansion. For intermediaries, it reduces surface area.

What Vidhya Srinivasan called an “expansionary moment” is expansionary for Google. For companies that sit between the search query and the transaction, it is the opposite.

The Dual Compression Facing Lead Aggregators

Lead generation models are encountering pressure from both sides simultaneously.

Supply-Side Compression

Seer Interactive measured a 61% decline in organic CTR on queries with AI Overviews – across 3,119 queries and 25.1M impressions over 15 months. Bain reported that 60% of searches now end without a click, rising to 77% on mobile. Media leaders project sustained search referral decline over the next several years.

The result is not the elimination of intent, but the reduction of distributable clicks. The raw demand still exists. The path it takes to reach an intermediary is narrowing.

Demand-Side Compression

At the same time, buyers are gaining direct routing options through structured integrations like UCP. Cost-per-click inflation continues in high-LTV verticals, with insurance CPCs exceeding $900. Performance transparency is increasing scrutiny on lead quality and incrementality. And platform-native formats are reducing reliance on third-party intermediaries altogether.

The traditional arbitrage spread – traffic acquisition cost versus lead monetization – is narrowing from both ends. This is structural, not cyclical.

The Competitive Environment Is Broader Than Search

This is not a Google-only dynamic.

ChatGPT introduced ads and conversational commerce with 800M+ users and instant checkout already live through Shopify. Social platforms increasingly compress discovery and transaction into single environments – TikTok Shop alone is projecting $20B+ in gross merchandise value. Retail media networks capture transactional product search. Streaming platforms absorb upper-funnel brand budgets, with Netflix on a $3B+ ad revenue trajectory.

Across each of these environments, the pattern is the same: closed-loop ecosystems are expanding, and the intermediary comparison layer becomes less central unless it controls something the ecosystem cannot provide on its own.

What Becomes Structurally Defensible

The most exposed positions are generic comparison content, SEO-dependent traffic models, shared lead routing without differentiation, and static rate or offer aggregation. These are the assets AI replicates most easily and platforms absorb most quickly.

The more durable positions share a common characteristic: they involve something an AI agent needs but cannot independently generate.

Proprietary data. Claims history, outcome data, real-time pricing, authenticated credit profiles. This information is non-public, dynamic, and fenced behind permissions. An LLM cannot scrape what it cannot access.

Transaction rails. Embedded checkout, pre-qualification engines, UCP integration, billing and settlement infrastructure. AI agents need rails to ride on.

Exclusive supply. Legal exclusivity contracts with carriers or providers that block direct-to-AI access. If an agent cannot reach a provider without going through your exchange, you remain in the path.

Regulated infrastructure. TCPA compliance, CMS enrollment rules, state licensing requirements, physical verification of service providers. AI cannot independently assume regulatory liability or verify that a roofer is insured and local.

The shift is from content advantage to infrastructure advantage.

Vertical Implications

The pattern is consistent across high-CPC verticals. In insurance, the defensible position moves from generic listicles toward real-time API pricing exchanges and compliance infrastructure, with revenue shifting toward agency economics and policy bind. In banking and finance, it moves from static rate tables toward authenticated identity and embedded pre-qualification, with revenue shifting toward success fees on funded outcomes. In home services and legal, it moves from shared leads toward operational control – scheduling, dispatch, verified reviews – with revenue tied to booked appointments or job value. In telco and energy, it moves from generic availability lists toward address-level data accuracy and billing complexity, with revenue shifting toward lifecycle management.

In each case, the underlying question is the same: are you selling a click, or are you controlling the outcome?

The Valuation Implication

Public and private markets increasingly distinguish between traffic-dependent media models, infrastructure or exchange platforms, vertical SaaS operators, and licensed or renewal-driven businesses. The multiples reflect the distinction clearly.

Businesses that control proprietary data, transaction rails, or recurring relationships command structurally higher valuations than those dependent on organic arbitrage. A media model built on SEO trades at a fraction of what a vertical platform with first-party data and recurring revenue commands.

The strategic question is no longer how to restore traffic. It is whether the business can evolve beyond traffic dependency entirely.

The Diagnostic: Five Signals of Structural Exposure

For operators and investors evaluating exposure, five signals indicate the arbitrage model is already under pressure:

- NavBoost erosion – navigational queries in your category are increasingly satisfied on-page, and users skip the intermediary site.

- Zero-click dominance – mobile zero-click rates above 80% in your core query categories.

- Efficiency collapse – LTV-to-CAC ratio dropping below 3.0 as acquisition costs rise faster than monetization.

- Direct routing growth – increasing “direct-to-provider” click share in AI Mode results, bypassing comparison surfaces.

- Referral gap – LLM referral traffic replacing less than 5% of lost search volume, meaning new discovery channels are not compensating for search decline.

If three or more of these apply, the transition window is shorter than it appears.

Strategic Implication

This is not a call to abandon lead generation. It is a call to redefine what kind of business a lead generation company actually is.

Traffic arbitrage is being compressed. Infrastructure ownership is being repriced upward. The transition window is open, but it will not remain open indefinitely.

The question for operators and investors is not whether traffic declines. It is whether the business model evolves before dependency becomes irreversible.

Repositioning requires architectural decisions, not marketing optimizations: converting traffic into authenticated identity, building machine-readable offer infrastructure, owning eligibility and qualification logic, shifting monetization toward outcomes, and increasing control over the transaction moment.

About SAVD

SAVD works with enterprise operators and institutional investors to diagnose structural exposure across high-CPC lead generation models. Our focus is business model durability – not traffic recovery.

We are developing an agentic enablement layer designed to strengthen lead generation funnels through earlier eligibility resolution, structured offer integration, and clearer downstream performance visibility.

For operators and investors evaluating structural exposure, we welcome the conversation.

This analysis draws on Google’s 2026 Ads & Commerce letter, Seer Interactive CTR research, Bain zero-click data, and market observations across insurance, financial services, home services, and telco verticals.

Related Reading

Leaving Google to Fix the $200 Billion Coordination Problem

Stay Connected Follow SAVD on LinkedIn for ongoing analysis of structural shifts in performance marketing and lead generation.